Crypto

Examining The Nixon Shock Decisions That Would Lead To Bitcoin

This is an opinion editorial by Wilbrrr Wrong, Bitcoin pleb and economic history enthusiast.

Aug. 15 marks the anniversary of Richard Nixon’s 1971 decision to sever the link of the U.S. dollar to gold. A recent book by Jeffrey Garten, “Three Days At Camp David,” gives an excellent behind-the-scenes look at the process that led to this decision. The ultimate shape of the policy shift was a mixture of Cold War geopolitics, domestic Republican vs. Democrat jockeying and Nixon’s obsession with his 1972 reelection.

In reading about this time period, it’s hard to escape the conclusion that Bretton Woods was a system of control that was predestined to fail due to an inherently poor incentive structure. The rules of Bretton Woods often required politicians and governments to act against their own interests, and impose economic pain on their own people in favor of other nations and international stability. As this system’s tensions came to a head in 1971, peoples’ lives and businesses became subject to the vagaries and competitions of international power politics.

Bitcoin presents a compelling alternative system in which the selfish incentives of actors strengthen the network and monetary policy is known by all. This certainty allows for long-term planning and stability, especially as power politics and questionable government policies continue in the current day.

The Fraying Of The Postwar Order

For all the valid criticisms that are leveled against the Bretton Woods system, it did provide stability in the aftermath of World War II. The U.S. pledge to convert dollars for gold provided confidence for the world to rebuild after the devastation of 1939-1945. During this period American business and technology reigned supreme.

But as 1971 came, all was not well in the free world. Bretton Woods had established a system of fixed exchange rates between currencies. These rates were no longer realistic, given the remarkable recoveries of West Germany and Japan, among others. Indeed, these static rates had played an important role in the growth of powerful export sectors in these previously war-torn countries. As these export-based economies grew, America’s trade surplus shrank, until in 1971 it made the turn to a trade deficit for the first time since 1893.

The trade deficit gave rise to domestic struggles. Competition from artificially cheap imports increased the power of labor unions, who pushed for higher wages and job security. Labor and management also fought over corporations making investments and sending jobs overseas, a practice which was incentivized by the dollar’s elevated purchasing power.

Added into the mix was fiscal profligacy from the federal government. Deficits were driven by the expansive social programs of the 1960s, but also by the U.S. role as military protector of the West. Along with the Vietnam War, America also bore the expense of its troops stationed in Europe.

A final bit of stress came from trade barriers put up by American allies. These barriers were erected in the 1950s, when allied economies were taking the first steps to recover. In 1971, these countries had made tremendous strides. However, since much of their recoveries were based on exports, they were highly resistant to lowering the trade barriers.

Taken together, the U.S. of 1971 was being shaken from its long period of unquestioned economic prosperity and facing the real rising issues of inflation and unemployment. Nixon held a strong belief that his previous loss in the 1960 presidential election was due to a badly timed recession, so he was highly motivated to keep the economy and jobs growing leading up to 1972.

The Players

Policy discussions in the summer of 1971 featured four key players:

Richard Nixon

Nixon was born to a poor family in California and worked his way to Duke University through a combination of grit and ambition. He started his political career by unseating a three-time incumbent in the House of Representatives and made a fast impression as an effective soldier in pushing Republican legislative priorities.

Nixon was chosen as vice president in 1952 because Dwight Eisenhower, a universally revered military legend, wanted to stay “above the fray,” and he wanted someone on his team who was willing to do the dirty work to fight political battles.

During the 1950s, Nixon built impressive foreign policy credentials, and became respected as a gifted geopolitical thinker. As president, he would concentrate on grand, unexpected initiatives that changed the rules of the game. One of his most proud achievements was his 1972 visit to Beijing, meant to split China off as a solid Soviet ally.

This diplomatic coup was announced on July 15, 1971, exactly one month before he closed the gold window.

Nixon’s main interests were in geopolitical strategy and the Cold War. When it came to economics, his primary concern was his fundamental belief that recessions are what causes politicians to be voted out. Garten explains in his book that Nixon’s biographer wrote, “Nixon repeatedly interrupted Cabinet meetings to go over the history of Republican defeats when the economy was in slow growth or decline.”

John Connally, Secretary Of The Treasury

Connally, a Democrat, was former governor of Texas. He was a charismatic and ruthless politician. He was nominated by Nixon at the start of 1971 to shake up his economic team and create allies in Congress.

An unabashed American nationalist, Connally saw the European allies and Japan as ungrateful for putting up trade barriers after the U.S. had provided for their military defense in the 1950s and ’60s. In describing the gold window decision, he told a group of distinguished economists, “It’s simple. I want to screw the foreigners before they screw us.”

Connally did not have a finance background, but he was a quick study and would come to rely on Paul Volcker to back him up on the details. His large personality would give him outsized influence leading up to August 1971 and he would aggressively lead political and international negotiations following Nixon’s announcement.

Arthur Burns, Chairman Of The Fed

Arthur Burns is remembered as the Fed chairman who failed to contain the inflation of the 1970s, but in 1971, he was one of the most respected economists in the nation, with experience across academia and government and he had many relationships with business leaders.

Burns came to the White House in 1968 as Nixon’s economic counselor and one of his most trusted confidants. In appointing Burns as Fed chairman in 1970, Nixon’s goal was to have an ally who would keep the economy strong, and bluntly, do what the administration told him to do. Nixon made many private remarks disparaging the “supposed” independence of the Fed.

The former allies would come into almost immediate conflict. Nixon strongly preferred lower interest rates and an increase in the money supply. Burns wanted to defend the dollar and refused to budge on interest rates.

Another point of contention was wage and price controls. Congress had recently passed a bill to give the president legal authority for these controls, however they went strongly against Nixon’s free-market philosophy. Burns angered Nixon with repeated speeches advocating for the extensive use of wage and price controls to keep inflation in check.

As the Camp David weekend approached in 1971, Nixon’s team realized they had to bring Burns on board with the administration’s new economic package. Closing the gold window was a dramatic new direction, and Fed opposition would fundamentally undermine the initiative.

Paul Volcker, Treasury Undersecretary For Monetary Affairs

Paul Volcker was relatively unknown in 1971, however over the following decades he would come to be known as one of America’s most trusted public servants. He cultivated allies across Congress and several presidential administrations through honest discussions, unimpeachable integrity and deep knowledge of the monetary system. Volcker and Connally would establish a close working relationship, despite disagreement on several issues.

Volcker’s personal notes from this time period contain an interesting passage, which can be contrasted with Satoshi Nakamoto’s famous passage from the white paper. Volcker wrote:

“Price stability belongs to the social contract. We give government the right to print money because we trust elected officials not to abuse that right, not to debase that currency by inflating. Foreigners hold our dollars because they trust our pledge that these dollars are equivalent to gold. And trust is everything.”

This is a high-minded sentiment, and it reflected Volcker’s personality well. However, Satoshi clearly believed that public officials would always break that trust eventually, since their incentives are often skewed heavily toward debasement. Certainly Nixon had a marked skew toward money printing.

Currency Turbulence In The Summer Of 1971

As early as 1969, Volcker made presentations to Nixon and others on potential modifications of Bretton Woods. Volcker put together a report which described four options. This report would shape the broad outlines of policy discussions leading up to August 1971.

Option 1: Unmodified Bretton Woods

This was presented for completeness’ sake, however it was not seriously considered. Tensions were rising, and officials could see a crisis on the horizon.

A simple reason for this option’s lack of feasibility was that the U.S. did not have the gold to pay for all dollars outstanding. U.S. gold holdings were $11.2 billion, but foreigners held $40 billion. At any moment there could be a run on gold.

A 1967 incident shows the high-level strains at the time. America and Britain threatened to withdraw troops in retaliation if West Germany demanded conversion of their dollars to gold. Bundesbank chairman Karl Blessing responded with the “Bundesbank Blessing letter” to assure the U.S. that West Germany would not seek gold conversion as a contribution to “international monetary cooperation.”

Option 2: Modified Bretton Woods

Favored by Volcker, this option would keep the fundamental structure of Bretton Woods, but it would make several modifications to address shortcomings:

- Pressure West Germany and Japan to revalue their currencies.

- Introduce a mechanism to give more flexibility in adjusting currency exchange rates, within limits.

- Aggressively negotiate for allied countries to lower trade barriers to U.S. exports.

- Make new agreements with allies to share the burden of defense costs.

This strategy may have worked, however without an impetus to force negotiations, it would be a slow and grinding process, and there could be a crisis in financial markets before tangible progress was made.

Option 3: Close The Gold Window

This is obviously the way things went, but it was seen as radical in 1969, and it did not come without risks. It was meant as a shock treatment to force allies to the negotiating table, but at the height of the Cold War, the West needed to maintain a unified front against the Soviet Union. In 1972 especially, Nixon was preparing for his Beijing trip and he did not want ongoing squabbles with his allies.

In addition, the competitive currency debasements of the 1930s were fresh in recent memory. The shock of this option carried the risks of capital controls, protectionism and the use of exchange rates as economic weapons.

Option 4: Devalue The U.S. Dollar Against Gold

In this case, the U.S. would unilaterally adjust the dollar-to-gold exchange rate, for example from $35 to $38 per ounce of gold. This option was also presented for completeness, but it was not given much consideration. Since exchange rates were fixed, foreign currencies would simultaneously be devalued against gold, and no advantage would be gained.

As with other options, this would require negotiations for an exchange rate realignment, and could lead to competitive devaluation. It would also effectively steal some of the wealth of American allies, since they had large dollar holdings. And it would give an advantage to the Soviet Union, with its large gold mines.

Nixon’s economic team continued to refine and debate options, however in May of 1971 financial markets forced the issue. A prominent group of West German economists called for a revaluation of the deutsche mark, which caused unsettlingly large amounts of money to start to flow out of the dollar into other currencies, anticipating a realignment of values. West Germany was forced to let the deutsche mark float, essentially abandoning its fixed exchange rate obligation. France, Belgium and the Netherlands demanded dollar-gold conversion, in amounts large enough to stoke fears of an uncontrolled run on gold. This period was described as “the death watch for Bretton Woods.”

The world looked to the U.S. for leadership on a response, but frankly, the Nixon administration did not have its act together. Officials tried to project stability, and reaffirmed the U.S. commitment to convert gold at $35/ounce. But internally, Nixon’s team had a fractious meeting at Camp David on June 26 — prior to the famous August meeting — which produced only conflict and competing views. In the following week, Nixon berated a meeting of his Cabinet. Paraphrased by his chief of staff, Nixon’s message was: “We have a plan, we will follow it, we have confidence in it … If you can’t follow the rule, or if you can’t get along with the Administration’s decisions, then get out.”

The Final Plan Takes Shape

Nixon designated Treasury Secretary Connally as the sole point of contact for the press. Throughout July, Connally spoke of calm and “steady as she goes,” while internally, he worked with Volcker and others on fundamental changes to the structure of the postwar economic order. Several Congressmen started proposing their own plans, and Connally urged Nixon to take the initiative. He told Nixon, “If we don’t propose a responsible new program … Congress will make an irresponsible one on your desk within a month.”

As the weekend of Aug. 13-15 approached, a serious new rumor reached Volcker’s desk. The U.K. had asked for “cover” for $3 billion of their reserves — a guarantee of the value of their holdings in gold terms, in case the dollar was devalued. This was actually a miscommunication — they had asked for a much smaller amount, less than $1 million. But the specter of a run on gold appeared very real as Nixon’s team reconvened at Camp David.

By this point Volcker’s original options had been fleshed out as a comprehensive program, with features meant to appeal to both capital and labor, and others to force the allies to the negotiating table. The main points were:

- Closing the gold window.

- 10% tariff on all imports.

- Wage and price controls.

- Removal of the excise tax on autos, to stimulate car sales.

- Resumption of the investment tax credit, to stimulate investment and growth.

- Federal budget cuts, to help control domestic inflation.

The main points were essentially decided before the Aug. 13-15 weekend. Nixon used the meeting to let all his advisors air their views, and feel as though they had been heard. The most contentious issues were the gold window, and wage and price controls. Interestingly, Arthur Burns argued strongly against closing the gold window, and almost succeeded in convincing Nixon of his view. Once the plan was set, though, the main substance of the weekend was in figuring implementation details, and planning the speech to present the plan to the nation.

The Aftermath

The domestic reaction to Nixon’s Sunday night televised speech was almost unanimously positive — from the stock markets to business and labor leaders. There was some criticism that wage and price controls would favor business over labor, but the import tariff placated labor, as protection against cheap imports. Democrats were caught off guard that Nixon had taken several of their ideas as part of his plan, thus grabbing the credit for them. But overall, the total plan was seen as a bold new direction which seized the economic initiative in charting a path forward.

The real test of Nixon’s plan would come with America’s allies. They were furious at not being warned in advance, and the tariff and exchange rate realignment would pose serious challenges for their economies. Tense negotiations would follow, with regular threats of retaliatory measures.

In December 1971 new fixed exchange rate levels were agreed, and the import tariff removed. However, most countries would not follow through on their commitments, and in 1973 a fully free-floating environment was established. The dollar would retain its global preeminence, especially with the advent of the petrodollar.

The U.S. economy was strong in 1972, and Nixon triumphed in the diplomatic arena, with trips to Beijing and Moscow. Nixon won a landslide reelection, and he and his wife topped a Gallup poll of “Most Admired Men and Women in the World.” Only later would he fall from the presidency through the disgrace of the Watergate scandal.

Wage and price controls were initially very popular, and appeared to be keeping inflation in check. However, they led to a large and unwieldy federal bureaucracy, and these controls were eventually scrapped in 1974. The resulting pent-up inflation would come to define much of the American economy through the 1970s.

Wen Stability?

What’s striking in reading through the history of high-stakes currency policy is that countries always seem to be riding the ragged edge of disaster. Following the Nixon shock of 1971, there were a regular series of crises. There was a dollar “rescue” in the Carter administration, followed by the Plaza Accords, Long-Term Capital Management (LTCM), 2008 and on and on.

Bitcoin is often criticized for its “volatility,” but national fiat currencies do not have the best track record in this respect. By contrast, Bitcoin’s network operation is stable and robust, and its value proposition is unambiguous. Temporary shocks like 3AC and Celsius pose no danger to Bitcoin itself, unlike the latest “threat to capitalism” from Lehman, Greece or whatever else is the current insolvent organization.

Bitcoin is a bottom-up system which allows regular plebs to store their own economic value, without having to rely on far-off political negotiations. As we stay humble and stack sats, Bitcoin provides stability for long-term planning and a high degree of certainty during crazy times.

This is a guest post by Wilbrrr Wrong. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

El Salvador’s Minister of the Economy Maria Luisa Hayem Brevé submitted a digital assets issuance bill to the country’s legislative assembly, paving the way for the launch of its bitcoin-backed “volcano” bonds.

First announced one year ago today, the pioneering initiative seeks to attract capital and investors to El Salvador. It was revealed at the time the plans to issue $1 billion in bonds on the Liquid Network, a federated Bitcoin sidechain, with the proceedings of the bonds being split between a $500 million direct allocation to bitcoin and an investment of the same amount in building out energy and bitcoin mining infrastructure in the region.

A sidechain is an independent blockchain that runs parallel to another blockchain, allowing for tokens from that blockchain to be used securely in the sidechain while abiding by a different set of rules, performance requirements, and security mechanisms. Liquid is a sidechain of Bitcoin that allows bitcoin to flow between the Liquid and Bitcoin networks with a two-way peg. A representation of bitcoin used in the Liquid network is referred to as L-BTC. Its verifiably equivalent amount of BTC is managed and secured by the network’s members, called functionaries.

“Digital securities law will enable El Salvador to be the financial center of central and south America,” wrote Paolo Ardoino, CTO of cryptocurrency exchange Bitfinex, on Twitter.

Bitfinex is set to be granted a license in order to be able to process and list the bond issuance in El Salvador.

The bonds will pay a 6.5% yield and enable fast-tracked citizenship for investors. The government will share half the additional gains with investors as a Bitcoin Dividend once the original $500 million has been monetized. These dividends will be dispersed annually using Blockstream’s asset management platform.

The act of submitting the bill, which was hinted at earlier this year, kickstarts the first major milestone before the bonds can see the light of day. The next is getting it approved, which is expected to happen before Christmas, a source close to President Nayib Bukele told Bitcoin Magazine. The bill was submitted on November 17 and presented to the country’s Congress today. It is embedded in full below.

This is an opinion editorial by Joakim Book, a Research Fellow at the American Institute for Economic Research, contributor and copy editor for Bitcoin Magazine and a writer on all things money and financial history.

I don’t.

That’s it. That’s the article.

In all sincerity, that is the full message: Just don’t do it. It’s not worth it.

You’re not an excited teenager anymore, in desperate need of bragging credits or trying out your newfound wisdom. You’re not a preaching priestess with lost souls to save right before some imminent arrival of the day of reckoning. We have time.

Instead: just leave people alone. Seriously. They came to Thanksgiving dinner to relax and rejoice with family, laugh, tell stories and zone out for a day — not to be ambushed with what to them will sound like a deranged rant in some obscure topic they couldn’t care less about. Even if it’s the monetary system, which nobody understands anyway.

Get real.

If you’re not convinced of this Dale Carnegie-esque social approach, and you still naively think that your meager words in between bites can change anybody’s view on anything, here are some more serious reasons for why you don’t talk to friends and family about Bitcoin the protocol — but most certainly not bitcoin, the asset:

- Your family and friends don’t want to hear it. Move on.

- For op-sec reasons, you don’t want to draw unnecessary attention to the fact that you probably have a decent bitcoin stack. Hopefully, family and close friends should be safe enough to confide in, but people talk and that gossip can only hurt you.

- People find bitcoin interesting only when they’re ready to; everyone gets the price they deserve. Like Gigi says in “21 Lessons:”

“Bitcoin will be understood by you as soon as you are ready, and I also believe that the first fractions of a bitcoin will find you as soon as you are ready to receive them. In essence, everyone will get ₿itcoin at exactly the right time.”

It’s highly unlikely that your uncle or mother-in-law just happens to be at that stage, just when you’re about to sit down for dinner.

- Unless you can claim youth, old age or extreme poverty, there are very few people who genuinely haven’t heard of bitcoin. That means your evangelizing wouldn’t be preaching to lost, ignorant souls ready to be saved but the tired, huddled and jaded masses who could care less about the discovery that will change their societies more than the internal combustion engine, internet and Big Government combined. Big deal.

- What is the case, however, is that everyone in your prospective audience has already had a couple of touchpoints and rejected bitcoin for this or that standard FUD. It’s a scam; seems weird; it’s dead; let’s trust the central bankers, who have our best interest at heart.

No amount of FUD busting changes that impression, because nobody holds uninformed and fringe convictions for rational reasons, reasons that can be flipped by your enthusiastic arguments in-between wiping off cranberry sauce and grabbing another turkey slice. - It really is bad form to talk about money — and bitcoin is the best money there is. Be classy.

Now, I’m not saying to never ever talk about Bitcoin. We love to talk Bitcoin — that’s why we go to meetups, join Twitter Spaces, write, code, run nodes, listen to podcasts, attend conferences. People there get something about this monetary rebellion and have opted in to be part of it. Your unsuspecting family members have not; ambushing them with the wonders of multisig, the magically fast Lightning transactions or how they too really need to get on this hype train, like, yesterday, is unlikely to go down well.

However, if in the post-dinner lull on the porch someone comes to you one-on-one, whisky in hand and of an inquisitive mind, that’s a very different story. That’s personal rather than public, and it’s without the time constraints that so usually trouble us. It involves clarifying questions or doubts for somebody who is both expressively curious about the topic and available for the talk. That’s rare — cherish it, and nurture it.

Last year I wrote something about the proper role of political conversations in social settings. Since November was also election month, it’s appropriate to cite here:

“Politics, I’m starting to believe, best belongs in the closet — rebranded and brought out for the specific occasion. Or perhaps the bedroom, with those you most trust, love, and respect. Not in public, not with strangers, not with friends, and most certainly not with other people in your community. Purge it from your being as much as you possibly could, and refuse to let political issues invade the areas of our lives that we cherish; politics and political disagreements don’t belong there, and our lives are too important to let them be ruled by (mostly contrived) political disagreements.”

If anything, those words seem more true today than they even did then. And I posit to you that the same applies for bitcoin.

Everyone has some sort of impression or opinion of bitcoin — and most of them are plain wrong. But there’s nothing people love more than a savior in white armor, riding in to dispel their errors about some thing they are freshly out of fucks for. Just like politics, nobody really cares.

Leave them alone. They will find bitcoin in their own time, just like all of us did.

This is a guest post by Joakim Book. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

This is an opinion editorial by Federico Tenga, a long time contributor to Bitcoin projects with experience as start-up founder, consultant and educator.

The term “smart contracts” predates the invention of the blockchain and Bitcoin itself. Its first mention is in a 1994 article by Nick Szabo, who defined smart contracts as a “computerized transaction protocol that executes the terms of a contract.” While by this definition Bitcoin, thanks to its scripting language, supported smart contracts from the very first block, the term was popularized only later by Ethereum promoters, who twisted the original definition as “code that is redundantly executed by all nodes in a global consensus network”

While delegating code execution to a global consensus network has advantages (e.g. it is easy to deploy unowed contracts, such as the popularly automated market makers), this design has one major flaw: lack of scalability (and privacy). If every node in a network must redundantly run the same code, the amount of code that can actually be executed without excessively increasing the cost of running a node (and thus preserving decentralization) remains scarce, meaning that only a small number of contracts can be executed.

But what if we could design a system where the terms of the contract are executed and validated only by the parties involved, rather than by all members of the network? Let us imagine the example of a company that wants to issue shares. Instead of publishing the issuance contract publicly on a global ledger and using that ledger to track all future transfers of ownership, it could simply issue the shares privately and pass to the buyers the right to further transfer them. Then, the right to transfer ownership can be passed on to each new owner as if it were an amendment to the original issuance contract. In this way, each owner can independently verify that the shares he or she received are genuine by reading the original contract and validating that all the history of amendments that moved the shares conform to the rules set forth in the original contract.

This is actually nothing new, it is indeed the same mechanism that was used to transfer property before public registers became popular. In the U.K., for example, it was not compulsory to register a property when its ownership was transferred until the ‘90s. This means that still today over 15% of land in England and Wales is unregistered. If you are buying an unregistered property, instead of checking on a registry if the seller is the true owner, you would have to verify an unbroken chain of ownership going back at least 15 years (a period considered long enough to assume that the seller has sufficient title to the property). In doing so, you must ensure that any transfer of ownership has been carried out correctly and that any mortgages used for previous transactions have been paid off in full. This model has the advantage of improved privacy over ownership, and you do not have to rely on the maintainer of the public land register. On the other hand, it makes the verification of the seller’s ownership much more complicated for the buyer.

Source: Title deed of unregistered real estate propriety

How can the transfer of unregistered properties be improved? First of all, by making it a digitized process. If there is code that can be run by a computer to verify that all the history of ownership transfers is in compliance with the original contract rules, buying and selling becomes much faster and cheaper.

Secondly, to avoid the risk of the seller double-spending their asset, a system of proof of publication must be implemented. For example, we could implement a rule that every transfer of ownership must be committed on a predefined spot of a well-known newspaper (e.g. put the hash of the transfer of ownership in the upper-right corner of the first page of the New York Times). Since you cannot place the hash of a transfer in the same place twice, this prevents double-spending attempts. However, using a famous newspaper for this purpose has some disadvantages:

- You have to buy a lot of newspapers for the verification process. Not very practical.

- Each contract needs its own space in the newspaper. Not very scalable.

- The newspaper editor can easily censor or, even worse, simulate double-spending by putting a random hash in your slot, making any potential buyer of your asset think it has been sold before, and discouraging them from buying it. Not very trustless.

For these reasons, a better place to post proof of ownership transfers needs to be found. And what better option than the Bitcoin blockchain, an already established trusted public ledger with strong incentives to keep it censorship-resistant and decentralized?

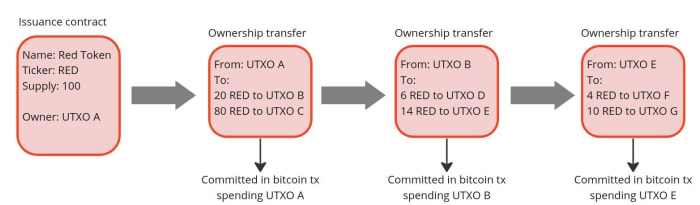

If we use Bitcoin, we should not specify a fixed place in the block where the commitment to transfer ownership must occur (e.g. in the first transaction) because, just like with the editor of the New York Times, the miner could mess with it. A better approach is to place the commitment in a predefined Bitcoin transaction, more specifically in a transaction that originates from an unspent transaction output (UTXO) to which the ownership of the asset to be issued is linked. The link between an asset and a bitcoin UTXO can occur either in the contract that issues the asset or in a subsequent transfer of ownership, each time making the target UTXO the controller of the transferred asset. In this way, we have clearly defined where the obligation to transfer ownership should be (i.e in the Bitcoin transaction originating from a particular UTXO). Anyone running a Bitcoin node can independently verify the commitments and neither the miners nor any other entity are able to censor or interfere with the asset transfer in any way.

Since on the Bitcoin blockchain we only publish a commitment of an ownership transfer, not the content of the transfer itself, the seller needs a dedicated communication channel to provide the buyer with all the proofs that the ownership transfer is valid. This could be done in a number of ways, potentially even by printing out the proofs and shipping them with a carrier pigeon, which, while a bit impractical, would still do the job. But the best option to avoid the censorship and privacy violations is establish a direct peer-to-peer encrypted communication, which compared to the pigeons also has the advantage of being easy to integrate with a software to verify the proofs received from the counterparty.

This model just described for client-side validated contracts and ownership transfers is exactly what has been implemented with the RGB protocol. With RGB, it is possible to create a contract that defines rights, assigns them to one or more existing bitcoin UTXO and specifies how their ownership can be transferred. The contract can be created starting from a template, called a “schema,” in which the creator of the contract only adjusts the parameters and ownership rights, as is done with traditional legal contracts. Currently, there are two types of schemas in RGB: one for issuing fungible tokens (RGB20) and a second for issuing collectibles (RGB21), but in the future, more schemas can be developed by anyone in a permissionless fashion without requiring changes at the protocol level.

To use a more practical example, an issuer of fungible assets (e.g. company shares, stablecoins, etc.) can use the RGB20 schema template and create a contract defining how many tokens it will issue, the name of the asset and some additional metadata associated with it. It can then define which bitcoin UTXO has the right to transfer ownership of the created tokens and assign other rights to other UTXOs, such as the right to make a secondary issuance or to renominate the asset. Each client receiving tokens created by this contract will be able to verify the content of the Genesis contract and validate that any transfer of ownership in the history of the token received has complied with the rules set out therein.

So what can we do with RGB in practice today? First and foremost, it enables the issuance and the transfer of tokenized assets with better scalability and privacy compared to any existing alternative. On the privacy side, RGB benefits from the fact that all transfer-related data is kept client-side, so a blockchain observer cannot extract any information about the user’s financial activities (it is not even possible to distinguish a bitcoin transaction containing an RGB commitment from a regular one), moreover, the receiver shares with the sender only blinded UTXO (i. e. the hash of the concatenation between the UTXO in which she wish to receive the assets and a random number) instead of the UTXO itself, so it is not possible for the payer to monitor future activities of the receiver. To further increase the privacy of users, RGB also adopts the bulletproof cryptographic mechanism to hide the amounts in the history of asset transfers, so that even future owners of assets have an obfuscated view of the financial behavior of previous holders.

In terms of scalability, RGB offers some advantages as well. First of all, most of the data is kept off-chain, as the blockchain is only used as a commitment layer, reducing the fees that need to be paid and meaning that each client only validates the transfers it is interested in instead of all the activity of a global network. Since an RGB transfer still requires a Bitcoin transaction, the fee saving may seem minimal, but when you start introducing transaction batching they can quickly become massive. Indeed, it is possible to transfer all the tokens (or, more generally, “rights”) associated with a UTXO towards an arbitrary amount of recipients with a single commitment in a single bitcoin transaction. Let’s assume you are a service provider making payouts to several users at once. With RGB, you can commit in a single Bitcoin transaction thousands of transfers to thousands of users requesting different types of assets, making the marginal cost of each single payout absolutely negligible.

Another fee-saving mechanism for issuers of low value assets is that in RGB the issuance of an asset does not require paying fees. This happens because the creation of an issuance contract does not need to be committed on the blockchain. A contract simply defines to which already existing UTXO the newly issued assets will be allocated to. So if you are an artist interested in creating collectible tokens, you can issue as many as you want for free and then only pay the bitcoin transaction fee when a buyer shows up and requests the token to be assigned to their UTXO.

Furthermore, because RGB is built on top of bitcoin transactions, it is also compatible with the Lightning Network. While it is not yet implemented at the time of writing, it will be possible to create asset-specific Lightning channels and route payments through them, similar to how it works with normal Lightning transactions.

Conclusion

RGB is a groundbreaking innovation that opens up to new use cases using a completely new paradigm, but which tools are available to use it? If you want to experiment with the core of the technology itself, you should directly try out the RGB node. If you want to build applications on top of RGB without having to deep dive into the complexity of the protocol, you can use the rgb-lib library, which provides a simple interface for developers. If you just want to try to issue and transfer assets, you can play with Iris Wallet for Android, whose code is also open source on GitHub. If you just want to learn more about RGB you can check out this list of resources.

This is a guest post by Federico Tenga. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.